Articles

Green Finance & Economy

Hard-Wiring Local Leadership: What COP30 Changes for Caribbean SIDS

For Small Island Developing States (SIDS), COP30 was less about announcing new promises and more about anchoring climate finance that can finally reach small, local projects quickly, fairly and without deepening debt.

Practitioner insights: Charlotte Reboul Paradis, Senior Manager in Policy & Sustainability Advisory, and Global Lead on Climate & Health at KPMG Islands Group, shares insights on the implications of these recent developments.

Introduction: the context of SIDS

"Protection of the vulnerable is non-negotiable". That line, echoed by the president of the Alliance of Small Islands States (AOSIS) ahead of COP30, captures today's reality: for SIDS, exposure to extreme weather events due to climate change is no longer a distant hypothetical threat. Hurricane seasons, heatwaves, coastline erosion, and pressure on food and water security are daily realities that the 39 small island countries around the world, home to 65 million people, must cope with.

What made Belém different was the sharper focus on the mechanism of climate finance: who controls it, how quickly it moves, and who bears the risk. Negotiations were turbulent, and finance remained a central fault line. Yet the fortnight delivered operational signals worth tracking, such as greater emphasis on locally led funds and banks, new attention to risk-sharing tools like parametric insurance, and tighter expectations around transparency and delivery. For SIDS, this shift from abstract ambition to locally-led access, delivery and risk-sharing is where COP30's real significance lies.

Why focus on SIDS?

While SIDS represent 0.5% of the world's surface, they host more than 20% of the world's biodiversity and 40% of global coral reefs. In addition to providing essential food supplies, healthy natural ecosystems are the heartbeat of the island's economy. Beaches and reefs are central to tourism, which averages roughly 30% of GDP across SIDS. Natural disasters, which affect different aspects of local communities, including tourism, cost SIDS approximately 18% of their gross domestic product (GDP), which is much higher than the world average of around 3%.

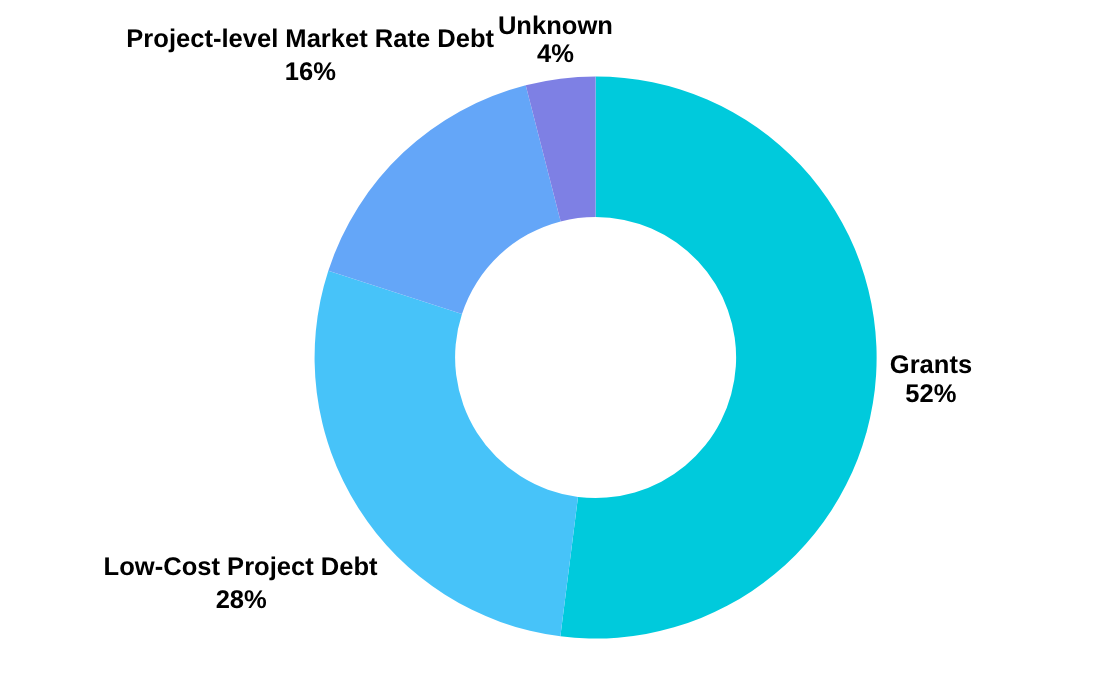

SIDS' unique exposure and vulnerability to the consequences of climate change make adaptation investment an economic necessity. Yet, the latest dedicated tracking carried out by the Climate Policy initiative (CPI) and the Global Centre on Adaptation (GCA) shows SIDS received just 0.2% of global climate finance for adaptation, representing a little over USD 2 billion annually (2021–2022), despite assessed needs of about USD 12 billion per year, six times the current amount for adaptative climate finance. Additionally, this extreme climate-related vulnerability is exacerbated by challenging financial conditions. Financial indicators point to "impending or deepening debt crises" in more than 70% of SIDS. In 2021-2022, around 44% (or USD 891 million) of adaptation finance to SIDS arrived as debt, compounding their economic burden and vulnerability even further. This economic posture prevents them from investing in essential mitigation, capacity-building and adaptation.

Figure 1: SIDS Adaptation Finance by Instrument, Average 2021–2022 (in millions USD)

Source: author's graphic composed with data from the GCA (2025).

Access and delivery of climate finance

For SIDS, the core problem is not only how much money there is on the table, but whether finance exists at the right scale and can be delivered fast enough to match the need. Although SIDS are responsible for less than 1% of global greenhouse gas emissions, they are among the most affected by climate change. International public adaptation finance to SIDS is still dominated by multilateral development banks, which provide around 60% of these flows. Bilateral governments contribute a far smaller share (31%), while multilateral climate funds account for just 7%. Flows are highly concentrated within ODA-eligible SIDS: with 10 small islands receiving 67% of total tracked adaptation finance. Overseas territories, such as the British Virgin Islands, face an additional hurdle, as their constitutional status makes them ineligible for major climate funds such as the Adaptation Fund or Green Climate Fund. And even when countries are eligible (and funds exist), access is often delayed by limited institutional capacity, fragmented and overlapping development finance interventions, small ticket sizes, lack of technical capacity and high transaction costs. This suggests that challenges to access finance and the capacity to deliver it, not only volume, are the real bottlenecks for SIDS.

What was different at COP30 for Caribbean SIDS?

What struck me this year is that, unlike earlier COPs that leaned on pledges, COP30 shifted the centre of gravity toward local or regional leadership for innovative approaches to access and delivery of climate finance.— Charlotte Reboul Paradis

For Caribbean SIDS, this shift towards locally-led access and delivery is not just rhetorical. Over the past few years, governments and regional institutions have built their own funds, banks, and platforms to create, bundle and execute projects. COP30 did not invent these tools, but it has raised the stakes: in addition to adapting international financial tools to the needs of small islands, it has become increasingly clear that locally-centred instruments are essential to move faster, reach smaller projects fairly, and avoid deepening already-high debt burdens.

Local and regional finance instruments

Recent years have seen progress in putting SIDS, instead of distant intermediaries, at the centre of climate finance decisions. In the Caribbean, a new generation of locally-led instruments is emerging that does more than simply "channelling the funds", but rather provides governments and regional institutions with their own platforms to develop, aggregate and roll out projects.

The British Virgin Islands' (BVI) Climate Change Trust Fund (VICCTF) is one example. Established by national law as an independent locally governed fund, it is designed to mobilise international contributions alongside domestic revenues and to channel small, fast grants to priority adaptation and mitigation projects. By acting as a single "front door" for proposals, the fund can bundle community-scale projects, meet access standards, and move money more quickly than fragmented channels. For the overseas territory that is ineligible to major climate funds, the VICCTF also provides a credible vehicle for bilateral partners and philanthropic donors, with environmental and social safeguards and fiduciary rules anchored in domestic legislation. First established in 2015 through the Virgin Island Climate Change Trust Fund Act, recent government updates have focused on fully re-establishing and operationalising the fund for as early as 2026. This recent push reflects lessons from Hurricane Irma, which exposed capacity gaps between committed finance and timely delivery.

Barbados' state-owned Blue Green Bank represents a complementary model: a dedicated national development finance institution able to mobilise concessional capital, blend it with domestic resources and on-lend for climate-resilient infrastructure and blue economy investments. First announced at the Summit for a New Global Financing Pact in Paris in 2023 and legislated through the 2024 Blue Green Act, the bank is currently finalising its governance to become operational. Once running, it aims to finance USD 250 million of green investments in affordable homes, hurricane-resilient infrastructure, and the electrification of public and private transport, in alignment with the Paris agreements and with Barbados' NDC and development plans. As pipelines mature, the bank is expected to co-finance projects across the region, allowing notably Jamaica and other SIDS to plug into a shared platform for standardised, locally-led project origination and risk-sharing, which will benefit many small tickets that would otherwise struggle to reach scale.

At the regional level, the new CARICOM Platform for Catalysing Resilience and Climate Action, announced this past June, pushes the same logic further. Chaired by Barbados and hosted at the Caribbean Development Bank, the platform uses Green Climate Fund (GCF) Readiness resources to develop a regionally-led investment instrument able to identify and deliver country-focused "game-changing" projects while coordinating a regional approach to climate change resilience with a focus on clean energy, resilient transport, water and food security. With an emerging coalition of Caribbean governments, a regional steering committee, a dedicated secretariat and technical working groups, the platform aims to aggregate national projects into regional programmatic packages. Crucially, this approach will reduce transaction costs and align contributors behind a common framework, which will improve the pooling of international investments. In addition, the platform seeks to mobilise innovative instruments that do not add to already-high debt burdens, while providing technical assistance to small administrations, in turn improving delivery models.

Taken together, these three instruments illustrate how locally-led finance in the Caribbean is moving from concept to institutional reality, creating national and regional mechanisms that facilitate access to international funds, organise and distribute the kind of projects SIDS need to mitigate and adapt.

Local and regional instruments have the potential to ensure financing better aligns with local mitigation and adaptation needs, contributing to strengthening local climate finance ecosystems. Regional tools and platforms also bring scale to projects and pipeline, increasing attractiveness to institutional investors, both regional and international.— Charlotte Reboul Paradis

Innovative risk-sharing tools

Beyond new funds and banks, new instruments are also changing who bears the risk of climate change. Parametric insurance tools, such as the Caribbean Catastrophe Risk Insurance Facility Segregated Portfolio Company (CCRIF SPC), allow governments to purchase coverage that pays out automatically when pre-defined triggers (wind speed or rainfall intensity, for instance) are met. Because payouts are set on modelled loss rather than lengthy and costly post-damage assessments, funds can quickly be rolled out within days, providing essential liquidity for emergency response and early recovery. Since 2007, the CCRIF made a total of 82 payouts, which represent USD 483 million disbursed. Most recently, Jamaica received USD 92 million from the Caribbean insurance facility following the devastating effects of Hurricane Melissa. Additional piloting has also been announced through the Livelihood Protection Policy (LPP) to support households vulnerable to extreme weather events and typically unable to access traditional insurance.

Tools like the parametric insurance do not replace long-term adaptation, but they limit the fiscal shock from disasters and transfer part of the risk to global reinsurance and capital markets. They are an important complement to locally-led funds and banks that are aiming to scale-up investments while preventing the deepening of SIDS' debt burdens.

By transferring a portion of disaster risk to global reinsurance and capital markets, these tools make it easier for governments and investors to commit to longer-term resilience investments without fearing that the next storm will blow up their balance sheets.— Charlotte Reboul Paradis

Global momentum and renewed accountability

A wider shift in the global climate regime also makes COP30 different for SIDS. Ten years after the Paris Agreement, the new round of Nationally Determined Contributions (NDCs) submitted ahead of Belém has injected fresh urgency into how countries meet their goals. The UNFCCC's 2025 NDC synthesis report notes not only higher overall ambition but clearer treatment of the "means of implementation": adaptation finance, technology transfer, capacity-building, and approaches to loss and damages now figure more prominently, with adaptation and resilience included in roughly three-quarters (73%) of new NDCs. For SIDS, this is significant, it grounds their adaptation and resilience needs into a core architecture of global climate commitments, rather than in side agreements or voluntary initiatives.

Concurrently, expectations about clarity and accountability have tightened. Under the Enhanced Transparency Framework adopted in 2024, Parties must now submit biennial transparency reports (BTRs), with more flexibility for SIDS and Least Developed Countries, that track their progress against their NDCs. As the second round of BTRs roll in through 2025-2026, attention will shift from headline pledges to delivery metrics such as time-to-disbursement, the share of grants and guarantees, operations and maintenance of funding or the inclusion of vulnerable groups.

The evolving accountability regime raises the cost of underperforming on access and delivery, and creates new leverage for SIDS to demand climate finance at a faster, fairer rate, while ensuring alignment with real-world constraints.

What's next?

Belém did not solve the climate-finance equation; it changed the terms. The next twelve months will show whether locally governed funds and banks, parametric insurance and heightened global scrutiny will improve access to adequate, predictable finance for Caribbean SIDS to mitigate and adapt. For these mechanisms to succeed, international partners will need to support the standardisation and de-risking of small projects and fund delivery systems by channelling more concessional finance through national and regional vehicles that know their markets.